How Debt Management Affects Credit Score in USA 2026

Introduction: Let’s Talk Honestly About Debt

Let’s be real for a second: debt is stressful.

If you’ve ever opened your mailbox and felt your stomach drop seeing another credit card bill, or if your phone rings and you’re scared it’s a collector — you’re not alone.

How Debt Management Affects Credit Score in USA, Millions of Americans are in the same boat. In fact, the average household carries tens of thousands of dollars in debt. And when you’re buried under it, one question keeps haunting you:

👉 “If I join a debt management plan, what will happen to my credit score?”

I get it — because your credit score feels like your financial passport. Without it, buying a home, getting a car, or even applying for some jobs becomes harder. You don’t want to make things worse while trying to fix them.

So, let’s sit down (imagine we’re having coffee together ☕) and walk through this whole thing — what debt management is, how it affects your credit, and whether it’s the right move for you.

No jargon, no scary terms — just straight talk.

What Exactly Is Debt Management?

Think of Debt Management Plans (DMPs) as a “reset button” for your financial life — but not a magic one.

Here’s the deal:

- You work with a nonprofit credit counseling agency.

- They look at your full money picture: income, bills, debts.

- They negotiate with your creditors (usually credit card companies) to lower interest rates and fees.

- You make one single payment to the agency each month, and they split it among your creditors.

Basically, instead of juggling 5–6 different bills, you have just one payment.

💡 Important: This is not debt settlement (where you pay less than what you owe). Debt settlement can crush your credit. Debt management is about paying off your debt in full, but under better terms.

Okay, But How Does This Affect My Credit Score?

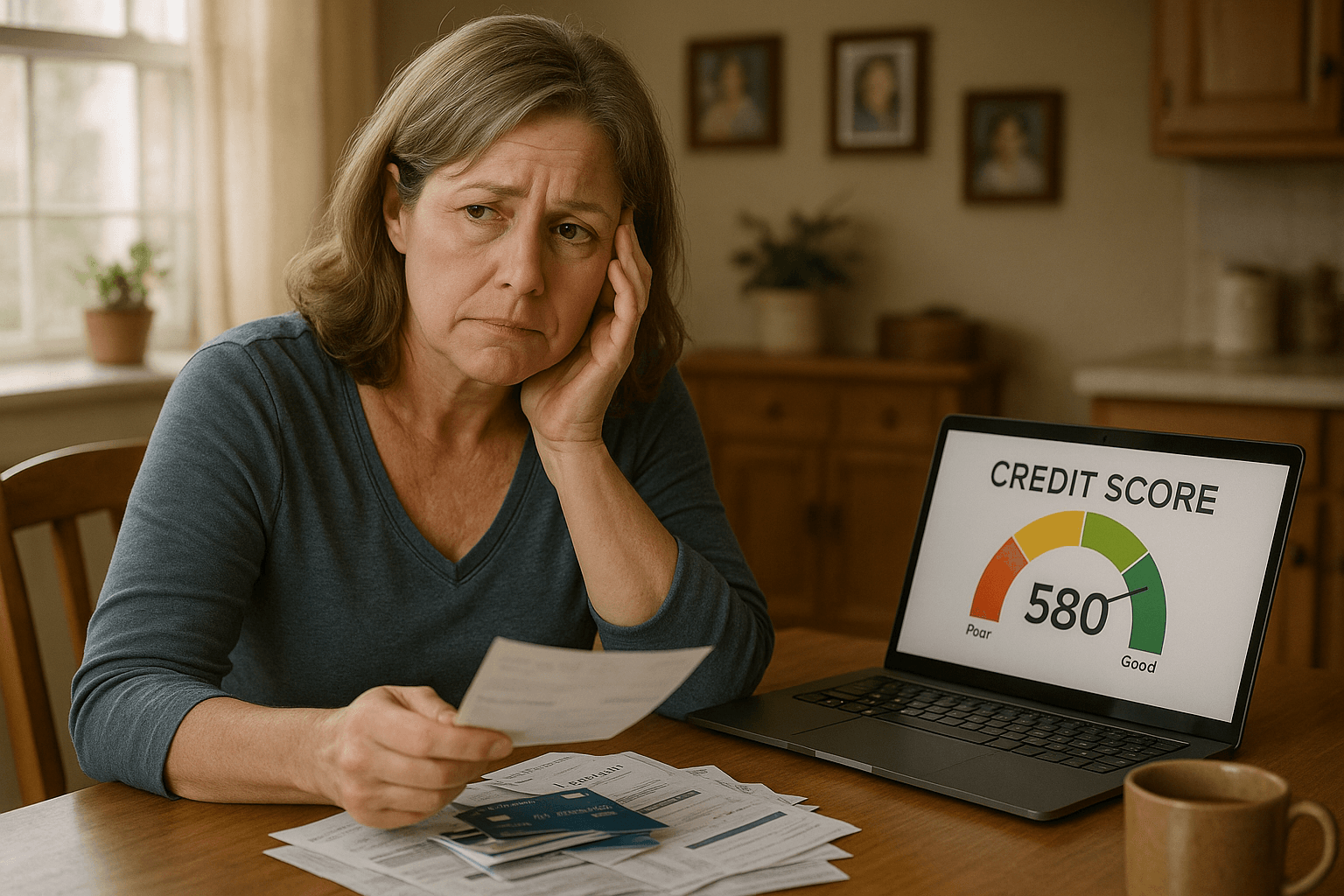

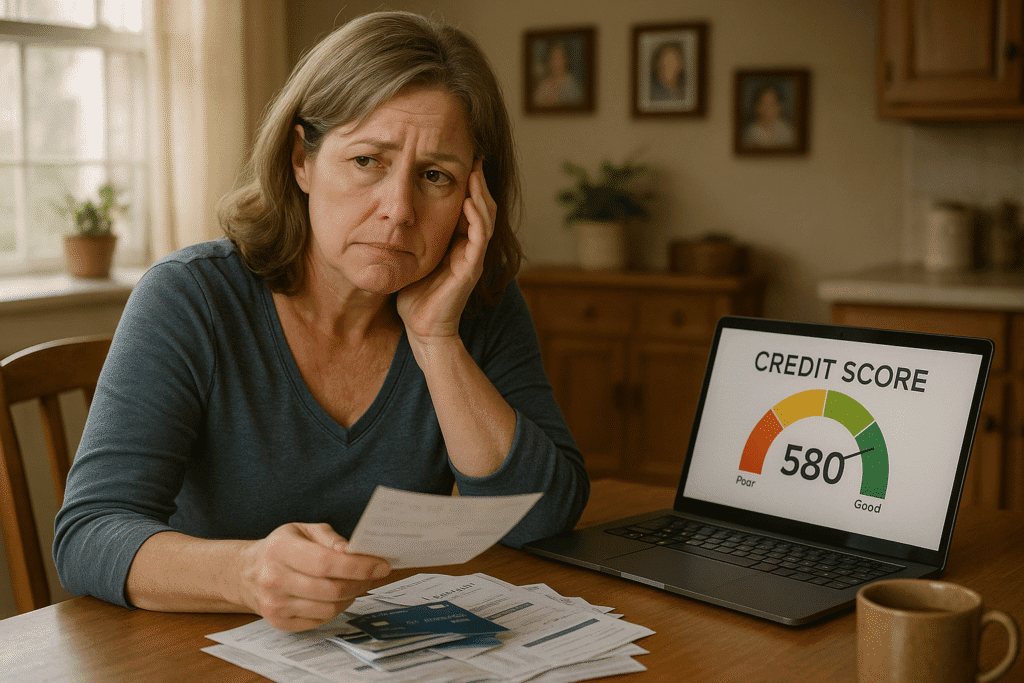

Here’s the truth: your credit score may take a small hit at first.

Let’s break it down into short-term vs long-term effects.

Short-Term (The “Ouch” Phase)

- Account Closures: Most creditors want you to close accounts when you join a DMP. This can shrink your available credit limit, which temporarily bumps up your “credit utilization ratio.” Translation: your score may dip.

- Credit Report Notes: Your report might say “enrolled in credit counseling.” It’s not as bad as a missed payment, but some lenders raise an eyebrow at it.

- Small Score Drop: Usually around 10–50 points in the beginning.

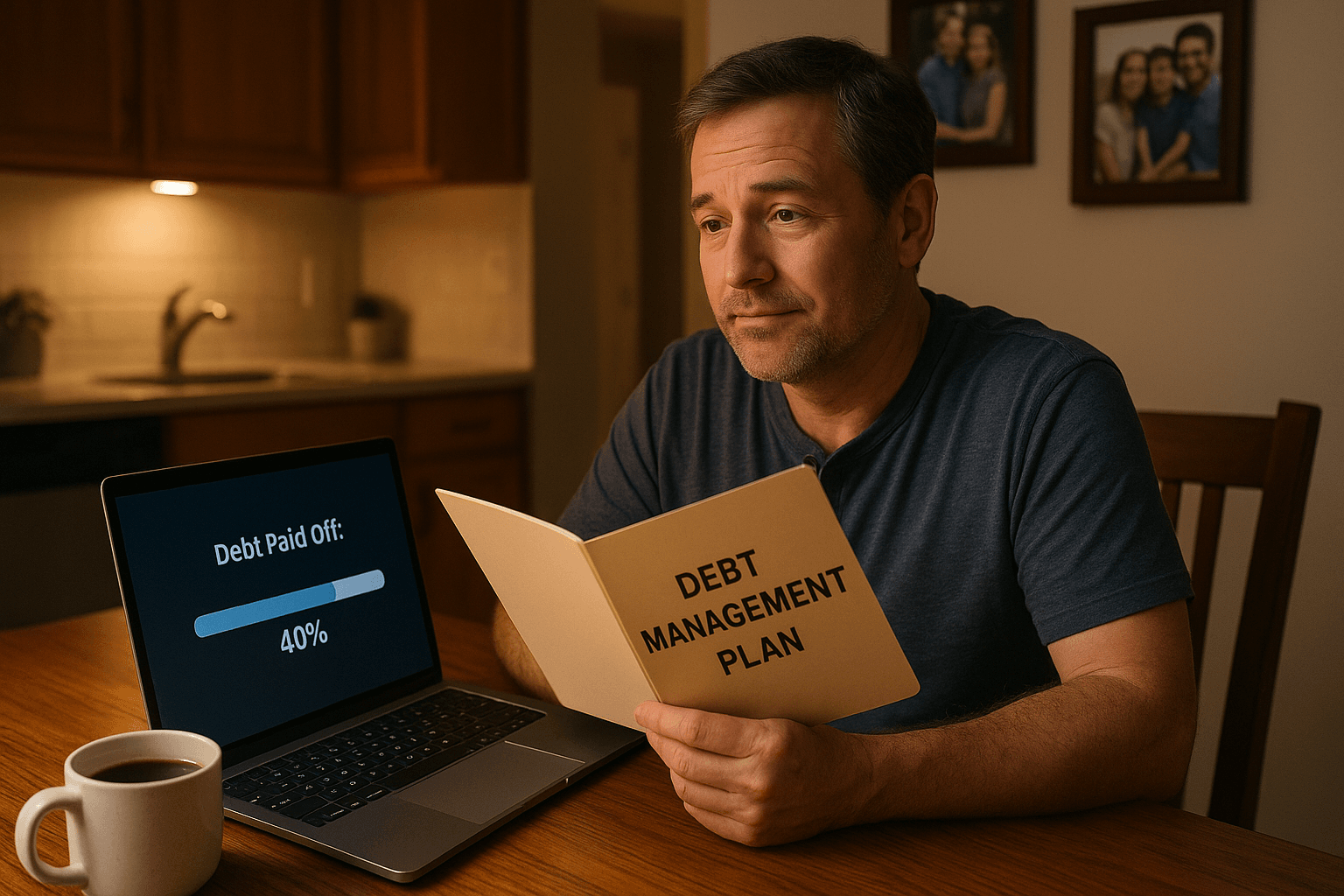

Long-Term (The “Relief” Phase)

Here’s the good news — if you stick with it, your credit score can actually climb higher than before.

- On-Time Payments: Every payment counts. Payment history makes up 35% of your FICO score.

- Less Debt = Healthier Score: As your balances go down, your credit utilization improves.

- Debt-Free Glow: Imagine how lenders see you once you’ve finished: no debt, steady payments. That’s powerful.

👉 So yes, there’s a little pain at first, but long-term it usually leads to a stronger, healthier credit score.

A Real-Life Example (Because Stories Hit Different)

Meet Sarah from Ohio.

- She had $18,000 in credit card debt across 5 cards.

- Her monthly minimum payments were eating her alive — over $600/month.

- Her score was 640.

Sarah joined a DMP:

- 3 of her cards were closed.

- Her interest rates dropped from 22% → 8%.

- Her new monthly payment became $400.

👉 At first, her score dipped to 615. She was nervous, even thought about quitting. But she stayed with it.

Fast forward 3 years later:

- She had paid off 70% of her debt.

- Her FICO score jumped to 710.

- She felt in control for the first time in years.

That’s what debt management can do — short-term sacrifice, long-term peace of mind.

Pros & Cons: Let’s Be Real

✅ The Good Stuff

- Consistent payments = better history over time

- Interest rates go down → debt gets paid faster

- Eventually improves your score

- Brings peace of mind (no more juggling 5 bills)

❌ The Not-So-Good Stuff

- Temporary dip in score when accounts close

- “In credit counseling” note may scare off some lenders

- You have to stick with it — no shortcuts

- Doesn’t cover mortgages or car loans (only unsecured debt like credit cards)

Tips to Protect Your Credit During Debt Management

Here are some “friend-to-friend” tips if you’re starting a DMP:

- Keep one card open (if possible) to maintain credit history. Use it lightly and pay it off each month.

- Pay everything else on time — rent, utilities, phone bills. Those matter too.

- Check your reports often (AnnualCreditReport.com is free). Watch your progress.

- Don’t take on new loans unless it’s truly necessary.

- Focus on the future. A 30-point dip now is nothing compared to the 100+ point gain later.

Alternatives If You’re Really Worried About Credit Score

Debt management isn’t the only path. Here are some others:

- Debt Consolidation Loan: One big loan to pay off smaller ones. Can help if your credit is good enough to qualify.

- Balance Transfer Card: Move debt to a 0% APR card. Great if your debt is smaller and you can pay it within the promo period.

- DIY Budgeting: Tighten expenses, boost income, attack debt on your own.

- Debt Settlement: Pay less than owed — but this kills your credit for years.

- Bankruptcy: Last resort. Wipes the slate, but leaves a big mark (up to 10 years).

FAQs: Quick Friend-to-Friend Answers

Q1: Does a debt management plan ruin my credit?

👉 Nope. It may lower it a little at first, but long-term it usually helps.

Q2: Can I buy a house while on a DMP?

👉 Possible, but harder. You’ll have better chances after finishing the plan.

Q3: Will lenders know I’m in a DMP?

👉 Some might see a note on your report, but it’s not as damaging as missed payments.

Q4: Which is better — debt management or debt settlement?

👉 For your credit score, debt management is way safer. Settlement can crush your score.

Q5: How soon will my score improve?

👉 Usually within a year of consistent payments, but big gains come after completing the plan.

Closing Thoughts (From Me to You)

Debt is heavy. It makes you lose sleep, fight with loved ones, even doubt yourself. But let me remind you of this: debt doesn’t define you.

Yes, debt management may sting your credit score for a little while. But it also gives you something way more valuable — a chance to breathe, a plan to follow, and the hope of being debt-free.

👉 Think of it like fixing a broken bone. It hurts while it heals, but in the end, you’re stronger.

If you’re considering a debt management plan, talk to a certified nonprofit credit counselor. They’ll guide you without judgment.

Remember — your credit score matters, but your peace of mind and future freedom matter more. ❤️

You May Also Like

Small Business Finance Tips USA 2026: A Complete Guide for Entrepreneurs

Debt Relief Options in USA 2026